It’s not personal, it’s strictly business.

Many RIAs struggle with profitability when they attempt to “be all things to all people,” which forces them to offer a wide range of services to clients of all shapes and sizes. As we have previously written, if you begin by defining your ideal client, your focused service offering will take care of itself—simply provide solutions to the unique needs of the specific client niche you are looking to serve. And once you have a firm grasp of the services you are offering, you can then determine the proper technology stack and organization structure. One way to help hone your service offering and determine what type of client experience you are hoping to deliver, is to perform a client segmentation exercise at your firm.

At its core, client segmentation is about analyzing the all-important question of, “How can our firm allocate its finite resources, spread between both people and technology, across an ever-expanding client base in a way that every client feels they are receiving our best service?” The simple fact is, we only have so many hours in a day to devote to our clients, and we unfortunately have revenue and profitability constraints to contend with as well. We simply can’t be all things to all clients. The 80/20 rule, which states that 80% of your revenue will come from 20% of your clients, applies broadly across our industry, and therefore should be top of mind for all RIA owners. Conducting a client segmentation exercise will ensure you are devoting the majority of your time to the right 20% of your client base.

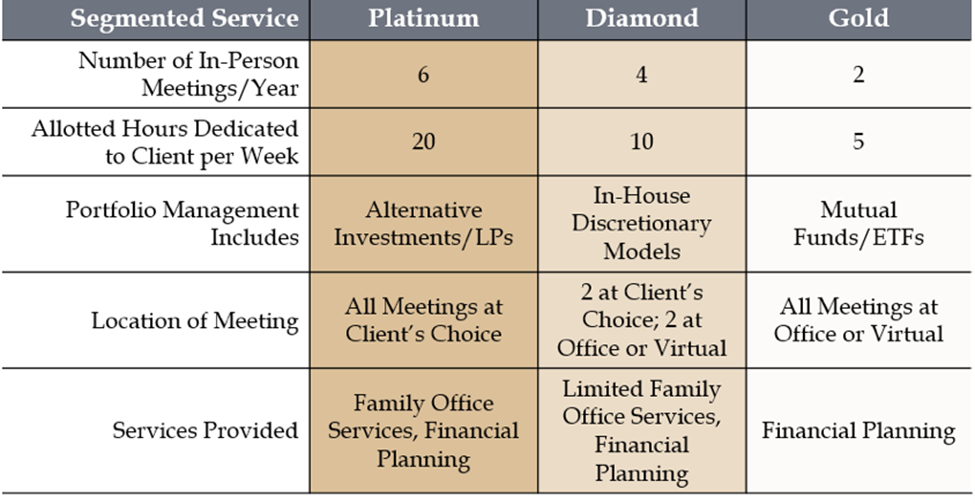

By dividing your clients into segments—A, B, C or Platinum, Diamond, Gold—whatever labels you want to apply, you can then create a service matrix that assigns how many in-person meetings vs. virtual meetings clients in each segment receive; how many touchpoints each segment receives via phone vs. email; what the standard response time for each client segment is; how many client events each segment can be invited to, etc.

Hypothetical client segmentation tiers

Some view this process of segmenting clients as controversial or even mean. That interpreted “meanness” comes from the belief that only money-grubbing RIAs that think profits before clients would ever consider slicing, dicing and ranking their client base. Others believe that segmentation leads to many clients being rejected services, and as an RIA they have a fiduciary duty to offer their services to any and all clients in need. Others equate client segmentation with providing lower service to smaller clients, and ask, “Shouldn’t all clients receive the best possible service I have to offer?” While I applaud the intent behind these misconceptions, as they are driven by a client-first mentality, I actually believe client segmentation is about serving more clients and serving thembetter.

If you were to provide every client with the same level of service, you could potentially cap out at 50 clients. If, on the other hand, you provide clients different service levels, based on their definition of “white glove service,” you can work with more clients and serve them according to their needs and desires. No one is saying that your largest client by AUM must be engaged in-person six times per year—maybe that client only wants to meet with you twice a year. Many RIAs mistakenly assume what every client wants from their advisor, instead of simply asking them. When assigning clients to certain segments, you must account for both quantitative (AUM, revenue, time needed to service the client, etc.) and qualitative (likeability, shared investment philosophy with their advisor, referability, etc.) aspects of the relationship, as well as asking them to define their idea of “good service.”

And yes, there is a profitability component to client segmentation—there has to be. You are, at the end of the day, running a business. If you continue to add more clients and you aren’t thoughtful about your service offering and the manner in which you deliver those services, you are going to need to hire more and more people, which is going to eat into profits and prevent you from having money to invest in the business. Your business is going to be hard pressed to grow without the ability to invest in the infrastructure needed to support that growth.

I do not believe client segmentation is evil. Client segmentation is about taking a step back and asking, “Does the level of service we are providing our clients make economic sense for our business?” This analysis will drive you to build a better client experience, allocate resources more appropriately, serve more clients, and have a better understanding of your firm’s business fundamentals. To borrow from Michael Corleone, “It’s not personal, it’s strictly (good) business!”

This article originally appeared on Wealthmanagement.com.