With RIA M&A activity at a frenzied pace, much has been written about how to best value an RIA business. Typically, a multiple is applied to either revenue or cash flow (profits). In my humble opinion, profits are all that matter. If two businesses are generating $1 million of revenue, with Business A running lean and producing $600,000 of bottom line earnings, while Business B can’t control expenses and is only generating $200,000 of earnings, it’s fairly clear that Business A is worth more to a potential buyer. (And any buyer partnering with the owner of Business B is opening themselves up to a world of hurt when that owner starts complaining about being “nickeled and dimed” as the buyer tries to incorporate higher profits into the business.)

I understand the simplicity and “rule of thumb” associated with revenue multiples, but most buyers who tout the ease associated with revenue multiples admit that they start with an earnings/profit margin number and then back into a revenue multiple, as Marty Bicknell of Mariner Wealth Advisors explained in this Financial Advisor Magazine article: “If we value the business based upon recurring revenue, that’s easy. We take the advisor’s revenue, plug it into our operating model metrics, and we can calculate a net cash flow number that we then convert to a revenue multiple.”

What is important to the buyer of the RIA is, “once we integrate this business into our firm, how much cash flow is it going to produce?” As Matt Cooper of Beacon Pointe described in the same Financial Advisor Magazine article, “Multiples of revenue don’t really work when valuing firms because they fail to take into account the cost of the structure needed to support those revenues. Free cash flow to the buyer is what is of value.” David DeVoe put it even more simply, by saying, “Multiples of revenue are dangerous, they’re horrible, they’re an infection into an organization that will destroy firms.”

Most RIA owners started their career within the wirehouse environment, where it was beaten into their heads that revenue was all that mattered. “Just go out and sell,” their sales manager would tell them on at least a weekly basis. And the fact that most recruiting packages offered to entice advisors to move their book of business from one wirehouse to another are all based on “production” (the wirehouse’s term for “revenue”) has led many RIA owners to undervalue the concept of profit. Once they make the mental shift from “I’m a financial advisor” to “I’m an owner of a financial advisory business,” they should also make the shift from focusing on revenue, to focusing on profits.

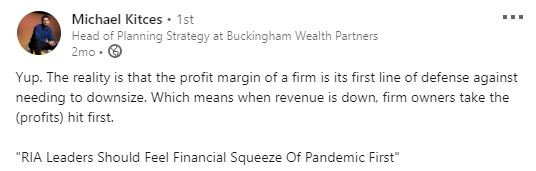

For those advisors who have fought this shift in mentality, the economic scare of the coronavirus has woken many business owners up to the benefits of a healthy profit margin. As Michael Kitces posted to social media in mid-May, as the potential economic impact of the pandemic began to weigh on RIAs, “The reality is that the profit margin of a firm is its first line of defense against needing to downsize.”

Much of the discussion around whether RIAs should or should not have applied for PPP loans has revolved around the liquidity/cash flow of each business and their ability to continue paying staff when revenues take a hit. With a renewed interest in bottom-line profits vs. top-line revenue, how should RIAs who are incentivized to make themselves as attractive to buyers as possible look to improve their bottom line as quickly as possible?

As we wrote in our article, Silver Linings: Using Crisis to Improve Your RIA’s Health, “there are only two sides to the profitability equation that you can manipulate in order to boost profitability: you can increase revenue, or you can decrease expenses.” Michael Kitces pointed out in this article from 2019:

“Increased size and revenues don’t necessarily result in increased profits, and scaling up in a time-intensive service industry isn’t always the most effective way to increase firm profitability. Luckily, alternative strategies can be employed to improve bottom-line results outside of growth for growth’s sake. And while these strategies don’t necessarily require capital, they do require a potentially painful gut check.”

At PFI Advisors, we call that “gut check” an Operational Diagnostic, where you conduct a full analysis of your back office systems and technology and ask yourself some tough questions:

- Are we overspending on technology tools that are more robust than we really need (the equivalent of buying a Ferrari to shuttle back and forth from the grocery store)?

- Have we underspent in certain areas, which has caused us to over-hire people to manually process things that could/should be automated?

- How can our systems run more efficiently?

- What workflows can be restructured?

- How can our collective systems integrate with one another better?

- What, if any, systems should be updated and/or replaced altogether?

In my opinion, this analysis needs to be done before hiring an investment banker to shop your business to interested buyers. The banker will undoubtedly thank you, as a healthier profit margin will make his or her job that much easier, as buyers will be that much more interested in speaking with you. With so much demand for recurring revenue businesses, it is the seller’s responsibility to showcase a steady, safe, and hopefully increasing profit margin, which ultimately results in a higher valuation for the seller. Ironically, if you drastically increase your profits, you may decide that you no longer want to sell, as you can enjoy the fruits of your labor in the form or greater cashflow/income – a true win-win!